VAT Reverse Charge for Construction

Posted on 13th May 2025 by Steven Burton

Navigating the complexities of VAT can be challenging, especially regarding specific regulations like the VAT Reverse Charge. Designed to combat VAT fraud, it shifts the responsibility for accounting for VAT from the supplier to the buyer in certain transactions. Whether you’re a supplier or a buyer, understanding when and how to apply the VAT Reverse Charge is crucial for compliance and effective cash flow management.

What is the VAT charge?

The VAT Reverse Charge applies to certain transactions within the UK where the supplier and the customer are VAT-registered and engage in construction works. Instead, the supplier still charges VAT on their invoice but also adjusts this so the “net” VAT impact is nil. This approach is designed to prevent fraud in the construction industry.

When does the VAT reverse charge need to be applied?

The VAT Reverse Charge is applied when both the supplier and the buyer are VAT-registered in the UK, and the transaction pertains to particular goods or services that are governed by reverse charge regulations, in predominantly, the construction industry The VAT Reverse Charge is only relevant when the customer is neither the end-user or an intermediary; in these situations, the supplier must apply VAT as normal, eg if CIS tax is charged then VAT Reverse Charge closely follows. The reverse charge is not applicable if the transaction involves entities that are not VAT-registered or do not fall into the specified categories.

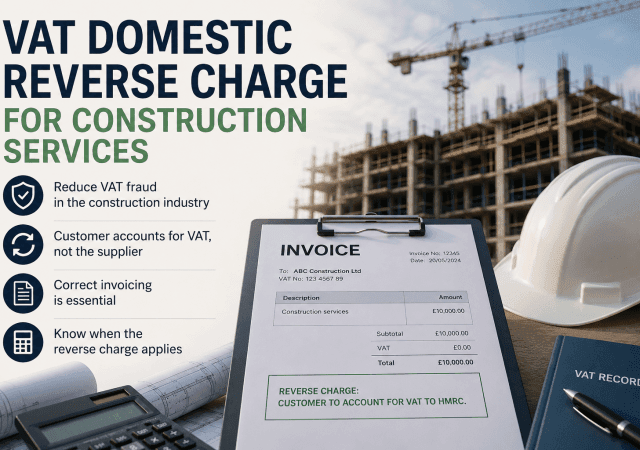

How to show the reverse charge on invoices?

When issuing an invoice under the VAT Reverse Charge, you still need to include VAT in the total amount charged to the customer, but your software should also deduct the VAT too (creating a “net” of nil VAT)

The invoice must include all standard information required for VAT invoices, such as your VAT registration number, the customer’s VAT number, and a description of the goods or services supplied. Additionally, include a note specifying the reverse charge, such as: “Reverse charge: VAT to be accounted for by the customer.” The VAT rate (e.g., 20%) should be shown for reference, but it should not be added to the total amount payable. Ensuring this information is clear and accurate is vital for compliance with HMRC requirements. We strongly recommend using accounting software like Xero, QuickBooks Online or Sage to account for this.

What to do if you make a mistake when applying the reverse charge?

If you make a mistake when applying the VAT Reverse Charge, it’s important to correct it as soon as possible to avoid potential issues with HMRC. Start by reviewing your records to identify the error, such as whether VAT was incorrectly charged. If you overcharged VAT, issue a credit note to the customer and adjust your VAT return accordingly. If VAT was under-accounted for, contact your customer to ensure they include the correct VAT amount on their return and update your records. Notify HMRC if the mistake affects your VAT return and follow their guidance for making adjustments. Regularly reviewing your processes and seeking professional advice can help prevent future errors. If you need assistance with your VAT Reverse Charge, contact our experts today!

Why is it important?

The reverse charge not only helps combat VAT fraud but also impacts cash flow management for businesses. For suppliers, it removes the obligation to collect and remit VAT on qualifying transactions. For buyers, it requires careful accounting to ensure VAT is correctly reported.

Ready to ensure your business is fully compliant with VAT Reverse Charge rules? Reach out to our team of experts today for tailored advice and guidance. Whether you need help understanding the regulations, adjusting your invoices or resolving mistakes, we’re here to support you every step of the way. Contact us now!